Wipro Q2 disappoints, earnings weakness to continue. Should you buy, hold or sell stock?

- Hot Stocks

admin

- 0

- 6 minutes read

Wipro’s revenue declined for the third consecutive quarter due to a broad-based decline in its key verticals

Wipro shares opened under pressure, falling over 3% on October 19, a day after the IT player reported a disappointing set of numbers for the September quarter.

Wipro clocked the weakest growth among peers. With the company’s profit and revenue declining and a weak Q3 guidance, analysts expect Wipro’s FY24 topline growth to be one of the lowest among Tier-1 IT services firms which include TCS and Infosys.

While most brokerages are not bullish on Wipro, they have not downgraded the stock, saying the valuation is fair.

Wipro shares were trading at Rs 392.80 on the National Stock exchange at 9:32 am.

The Bengaluru-headquartered company’s revenue declined for the third straight quarter due to a broad-based decline in its key verticals, including BFSI, communication, and manufacturing.

Its earnings before interest and tax (EBIT) margin and deal win total contract value (TCV) improved marginally.

Despite healthy deal wins, softness is expected to continue in the third quarter, as the company guided for a revenue performance in the range of -1.5 to -3.5 percent in constant currency, Motilal Oswal said.

“Given Wipro’s broader presence in the discretionary areas, the conversion is a challenge as enterprises are cautious and are reprioritising expenditures,” the brokerage said.

Also Read | Wipro’s Q2FY24 revenue slides to $2.7 billion, marking third consecutive quarterly decline

Outlook

Wipro‘s operating margins are expected to dip in the next quarter due to wage hike, followed by a sharp recovery in Q4, Motilal Oswal said in its report.

The resilience observed in the first half of FY24 is expected to provide support, and mitigate the potential downside impact on the full-year FY24 figures.

The operating leverage, a measure of how revenue growth translates into growth in operating income, miss in the third quarter will unlikely weigh on the FY24 margins.

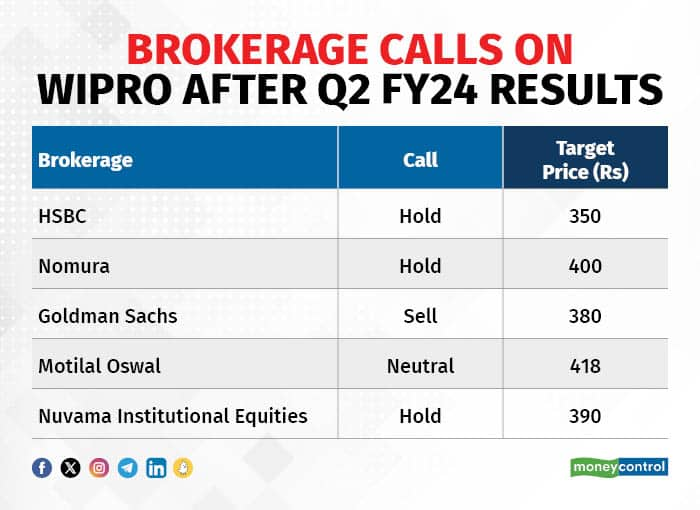

The brokerage has maintained a “neutral” call on the stock with a target price of Rs 418. It awaits further evidence of the execution of the IT firm’s refreshed strategy, and a successful turnaround from its struggles over the last decade before turning more constructive on the stock.

HSBC said that Wipro is undoubtedly impacted by demand slowdown and clear signs of market share loss.

“Wipro is stuck between an undemanding valuation and weak business traction,” analysts at HSBC said while maintaining a “hold” rating to the stock with a lower target price of Rs 350 a share.

Also Read | Reading the tea leaves: Takeaways from Big IT’s Q2 results

Nomura, too, stuck to its “hold” call on Wipro, with a target price of Rs 400, saying the company’s discretionary demand remains weak and the Q3 guidance showed that weakness is likely to persist.

According to Namura analysts, a margin improvement is unlikely in FY24. It has cut Wipro’s FY24-26 EPS estimates by 3-6 percent.

Goldman Sachs is bearish on Wipro, as it has a “sell” call on the counter with a target price of Rs 380.

According to the international brokerage firm, the IT firm’s Q3 revenue guidance of -3.5 to -1.5 percent QoQ indicates a further slowdown in revenue growth.

“We expect weak revenue growth outlook to result in further headwinds to near-term margins,” its analysts said, cutting FY24-26 EBIT/EPS estimates by up to 8 percent.

Follow our market live blog to catch all the live action

Wipro’s muted Q2 performance and disappointing Q3 guidance reaffirmed its troubles with converting deal-wins into growth, Nuvama Institutional Equities analysts said.

The brokerage expects Wipro to underperform peers, primarily due to its “intriguingly” low correlation between deal-wins and top-line growth.

“The stock’s inexpensive valuation and high dividend yield should limit downside potential in the medium-term,” it said, retaining the “hold” call with a target price of Rs 390.

Also Read | Wipro to merge five wholly-owned subsidiaries with itself

Disclaimer: The views and investment tips expressed by investment experts on Moneycontrol.com are their own and not those of the website or its management. Moneycontrol.com advises users to check with certified experts before taking any investment decisions.